628-2436 | Lic #01117537")

In the world of real estate, there are so many terms and phrases it can boggle the mind. 🤯 And agents tend to use a lot of “Realtor Speak” when communicating with clients.

We can’t help it. After so many years in the business, it’s just how we think and communicate with other professionals in the industry.

So forgive us for using our whacky terminology on you! To help out, below you will find many commonly used terms and real estate related definitions.

But if things aren’t clear or you still need answers to your questions, just reach out and we’ll be happy to help!

Welcome!

Welcome to our Frequently Asked Real Estate Questions page! Here you will find answers to some of the most common questions about buying and selling real estate.

Whether you are a first-time homebuyer or a seasoned investor, we have compiled a list of questions that can help you in your real estate journey.

Our goal is to provide you with the information you need to make informed decisions about your property.

If you have any additional questions, please don’t hesitate to contact us for more assistance. We look forward to helping you find the right property for your needs. Thank you for visiting!

Buying and Selling Real Estate

Are you looking to buy or sell a home?

If so, you may have a lot of questions about the real estate process. From finding the right property to understanding the paperwork involved, it can be overwhelming to navigate the real estate market.

To help make things easier, we’ve compiled a list of some of the most frequently asked real estate questions.

Whether you’re a first-time homebuyer or an experienced investor, these answers can help you get started on your real estate journey.

1. How do I find the right property for me?

The first step in finding the right property for you is to determine your budget and needs.

Consider the size of the home, location, and any special features you may want.

Once you have a better idea of what you’re looking for, start researching properties in your area.

You can search online, or contact a real estate agent for assistance.

2. What documents do I need to buy a home?

When buying a home, you’ll need to provide a few documents to your lender.

These include proof of income, bank statements, tax returns, and more.

Your lender will also require you to sign a purchase agreement, which outlines the terms of the sale.

Make sure to read through your purchase agreement carefully and ask questions if you don’t understand any of the language.

3. What is the process of selling a home?

Selling a home involves a few steps. First, you’ll need to list your property on the market and wait for offers.

Once you receive an offer, you’ll need to negotiate the terms with the buyer and sign a contract.

You’ll also need to complete the necessary paperwork and prepare the home for inspection.

After the inspection and appraisal are completed, you’ll need to close the sale and transfer the title.

4. What is the difference between renting and leasing?

The main difference between renting and leasing is the length of the agreement.

Renting typically requires a month-to-month agreement, while a lease is usually for a set period of time.

Renters are typically responsible for maintenance and repairs, while a landlord is usually responsible for these costs with a lease.

We hope this list of frequently asked real estate questions will be helpful as you navigate the real estate market.

If you have any additional questions, please contact a real estate professional for assistance.

Find the answers to your most asked questions about real estate. Click on the big + button to view the answer.

Financing

What is an Adjustable-rate mortgage (ARM)?

After an introductory period that could be 3, 5, 7, or 10 years, the interest rate on an adjustable-rate mortgage will be adjusted by the lender in accordance with current interest rates and your loan agreement.

For instance, a 5/1 ARM will have a fixed rate for the first five years, then the rate will vary based on a variety of factors. Your lender will explain the details before you accept the loan.

Typically, the interest rates on ARMs are lower for the fixed period which makes your payments more affordable during that period. However, the interest rate will generally go up along with your monthly payment after the rate is adjusted.

Homeowners consider ARMs riskier as you can’t predict what mortgage rates will be in the future.

What is Amortization?

The action or process of gradually writing off the initial cost of an asset.

Do you know what kind of mortgage you have? Do you know whether your payments are going to increase over time? 📈

“Amortization” is the term used for the schedule of mortgage installment payments over a period of time. Typically, a buyer’s amortization schedule is one payment per month over 15 or 30 years.

📢 Important:

📝 There are both adjustable and fixed-rate mortgages. With an adjustable rate, the lender can increase the rate on a predetermined schedule, which would impact your amortization schedule.

📝 With a fixed rate, your payments with remain the same for the life of the loan, unless you refinance or there are changes to taxes or insurance.

Leave a Reply

What is a bridge loan?

This short-term financing option can help you bridge the gap between buying a new home and selling your old one. It enables you to tap into your existing home equity before you’ve sold.

However, there are some issues to consider before you apply for a bridge loan:

👉 The interest rates and fees are usually higher than typical home loans.

👉 The equity from your current home will be used to secure the loan.

👉 The credit requirements are often greater for bridge loans than for standard financing.

If you think you may need to “bridge the gap” between buying a new home and selling your current one, give us a call. We can discuss your options and refer you to a lender who can help.

📲 925-628-2436

📩 info@guthriegrouphomes.com

Leave a Reply

What is a conforming loan?

A conforming loan is one that is limited to $647,200 for most of the U.S., which means you may be able to avoid the stricter requirements of a jumbo loan.

Loan limits vary over time and by location so you should check with your lender or Realtor for the latest information.

Other loan types include jumbo loans, FHA, and VA.

Leave a Reply

Conventional sale: When the property is owned outright and has no mortgage.

Conventional sales are often smoother transactions than those that require financing as there is no dependence on the buyer receiving a loan to purchase the property.

A conventional sale is not to be confused with a conventional loan. In this instance:

“Conventional” just means that the loan is not part of a specific government program. Conventional loans typically cost less than FHA loans but can be more difficult to get.

This may sound confusing, so just ask your Realtor to explain it to you if you’re not clear. ☺️

Leave a Reply

What is a credit score?

A number ranging from 300-850 that’s based on an analysis of your credit history.

Your credit score helps lenders determine the likelihood you’ll repay future debts.

You’ll need a score of 620 or better, but you’ll get better financing rates with a score of 720 or higher.

There is much more to know about credit and credit scores, so feel free to ask if you have specific questions.

To learn more about credit scores and credit reports, click here.

Leave a Reply

What is a Deed of Trust?

A Deed of Trust is like a mortgage. It is an agreement between a borrower (you) and a lender (a bank or other financial institution).

The lender gives you money to buy a house or other property, and you agree to repay the loan with interest, in regular payments.

The Deed of Trust also includes a clause that says if you don’t make the payments, the lender can take the property back.

Leave a Reply

What is a down payment?

The sum in cash that you can afford to pay at the time of purchase of a home or property.

A conventional loan down payment is usually 20% of the sales price, but other types of financing require as little as 3.5% to 15%. Some 0% down programs are also available.

A mortgage lender can tell you what types of loans you qualify for.

Leave a Reply

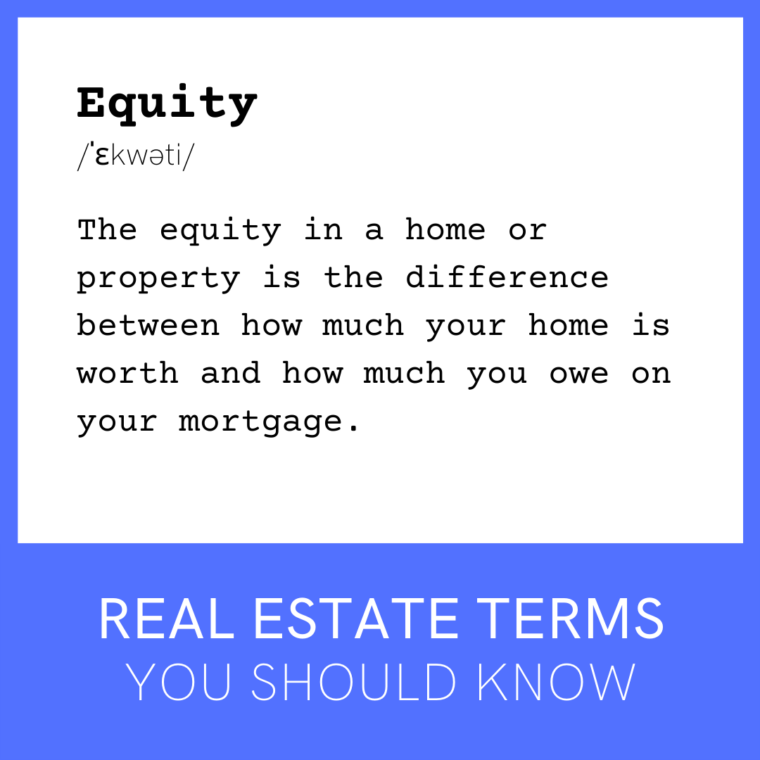

The equity in a home or property is the difference between how much your home is worth and how much you owe on your mortgage.

So if your home is worth $500,000 and you owe $450,000 on your mortgage, your equity in the home is $50,000.

See also home equity line of credit.

Leave a Reply

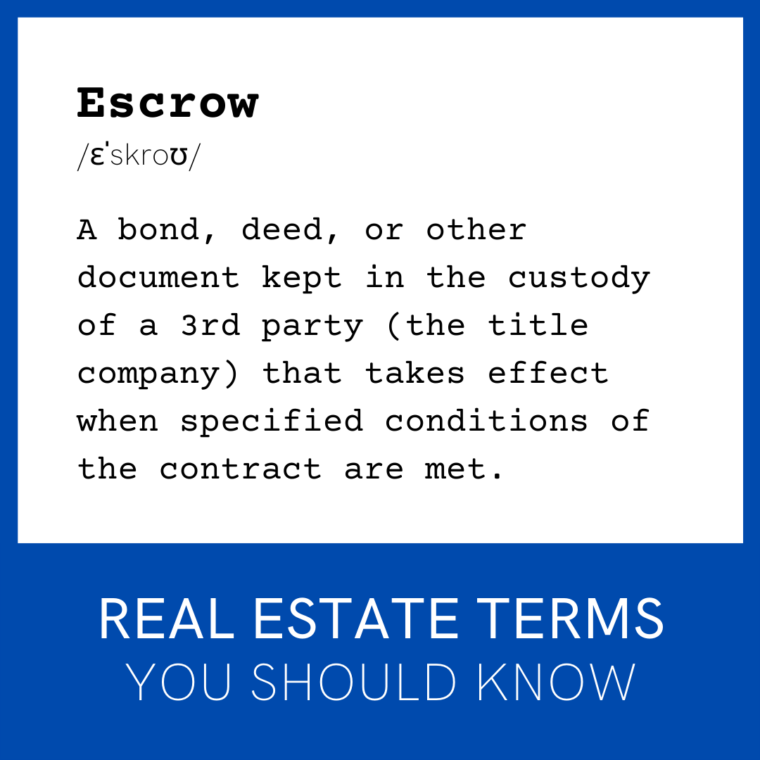

Escrow as it relates to real estate is a process of holding money and documents in a secure account while two parties complete a purchase.

Escrows are usually held by a Title and Escrow company.

This gives the buyer and seller peace of mind that the transaction is safe and that the buyer will not be able to take the money and run.

The escrow account ensures that the buyer has the necessary funds and that the seller will receive them when the transaction is complete.

See also close of escrow.

Leave a Reply

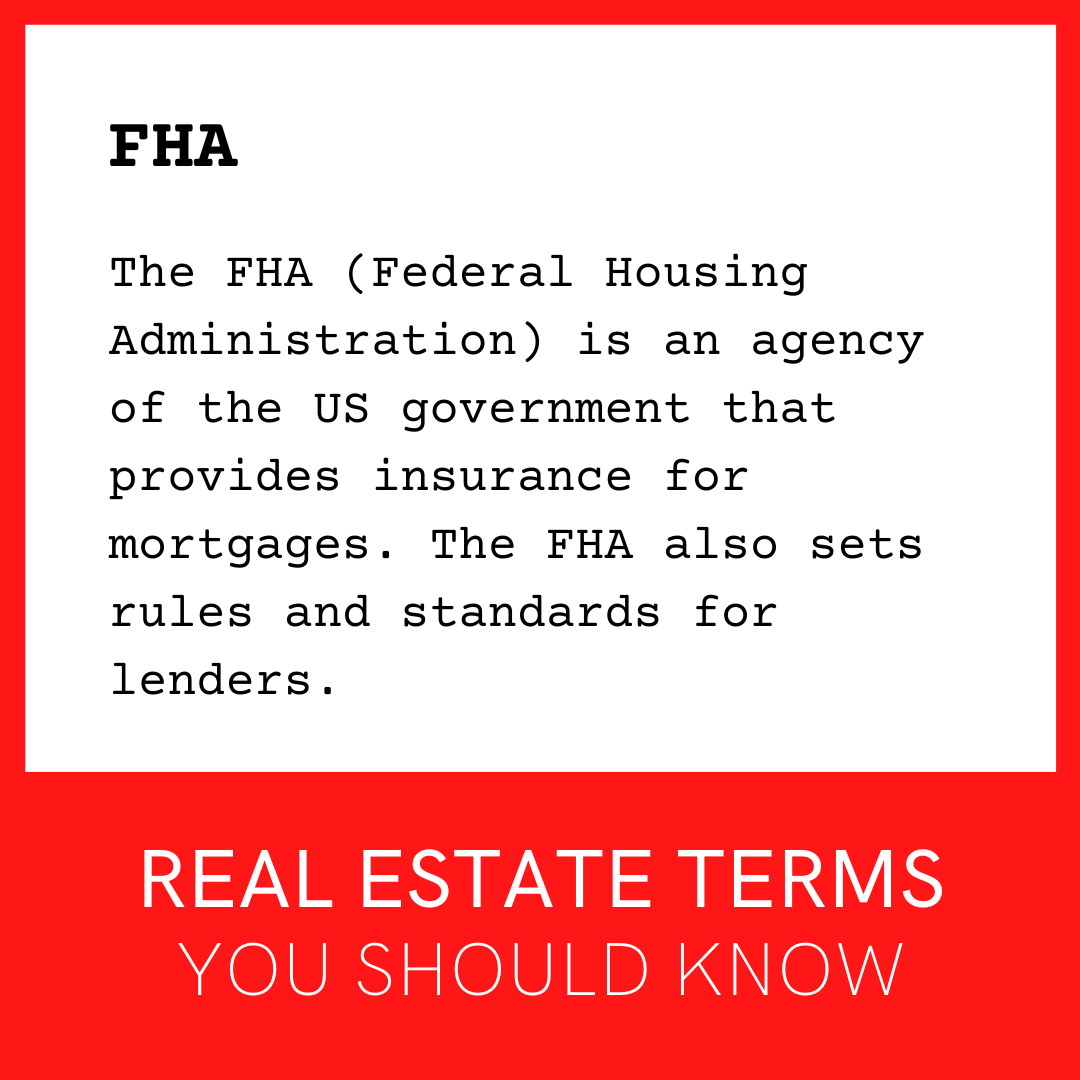

What is the FHA?

The FHA (Federal Housing Administration) is an agency of the US government that provides insurance for mortgages.

This insurance helps make it easier for people to get approved for a loan and makes it possible for them to get a loan with a smaller down payment.

The FHA also sets rules and standards for lenders to make sure that loans are fair and safe.

See also FHA Loan.

Leave a Reply

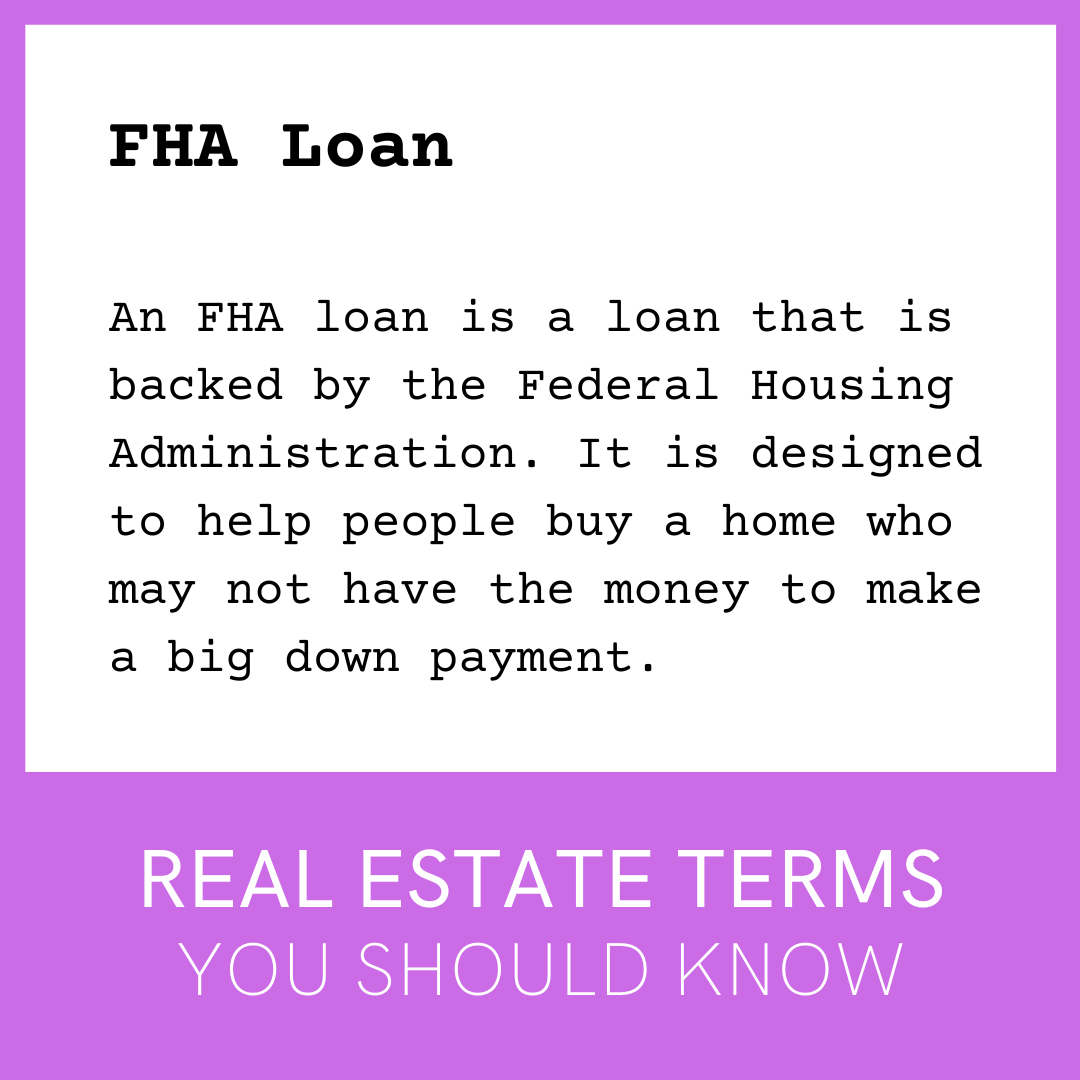

What is an FHA Loan?

A mortgage insured by the Federal Housing Administration – usually requires a good credit score and a down payment to qualify.

An FHA loan is a loan that is backed by the Federal Housing Administration. It is designed to help people buy a home who may not have the money to make a big down payment.

With an FHA loan, the borrower is able to make a smaller down payment and the government will help insure the loan, making it easier for the borrower to get approved.

Leave a Reply

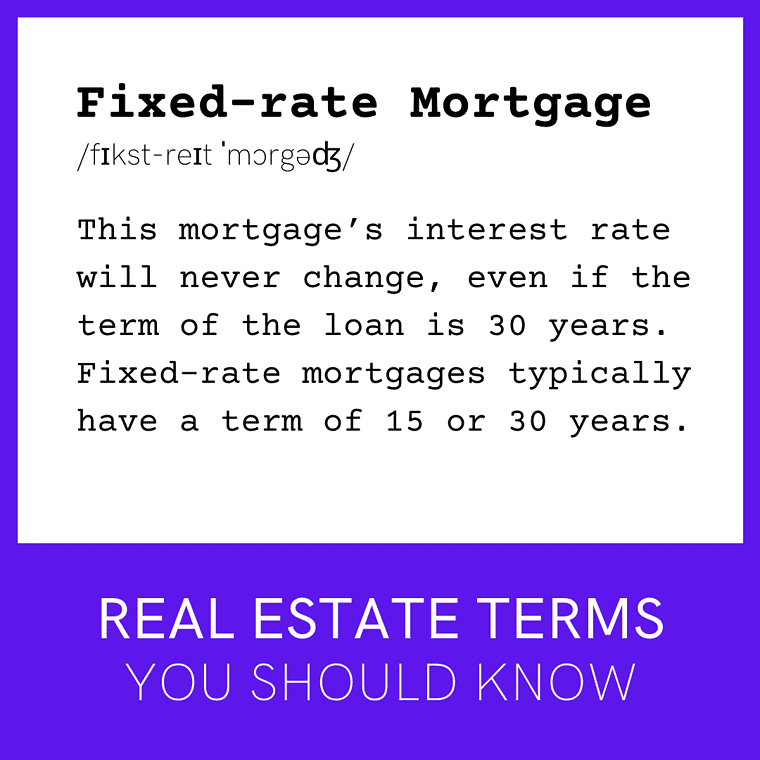

What is a fixed-rate mortgage?

This mortgage’s interest rate will never change, even if the term of the loan is 30 years.

Fixed-rate mortgages typically have a term of 15 or 30 years.

Homeowners prefer this type of loan as it has a lower amount of risk compared to variable-rate loans, and the monthly payment remains the same for the life of the loan.

Leave a Reply

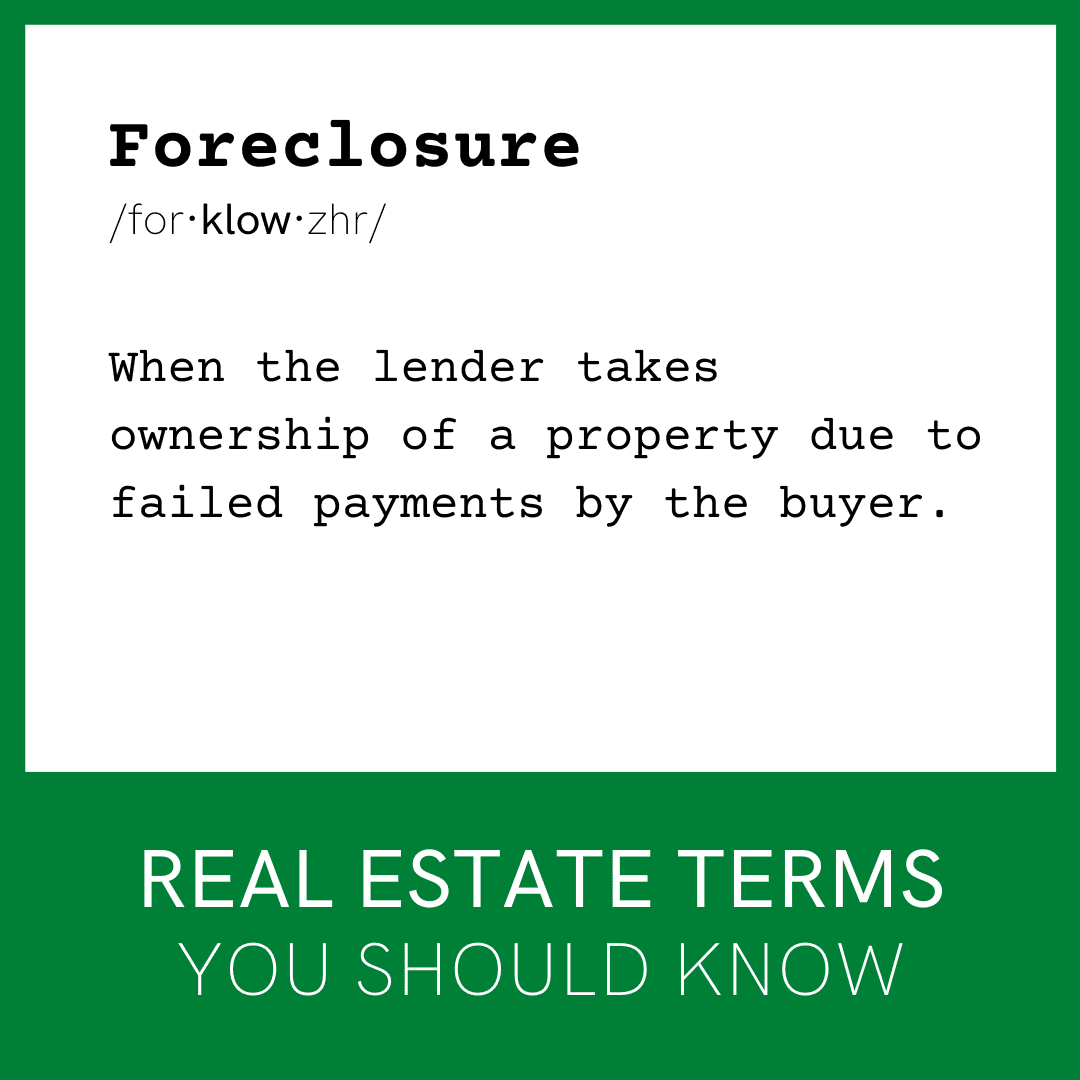

What is a Foreclosure?

When the lender takes ownership of a property due to failed payments by the buyer.

A foreclosure in real estate is when a homeowner stops making payments on their mortgage and the lender takes back the property.

The lender will then try to sell the property to recoup the money that was owed on the mortgage. Foreclosures can often be a lengthy and expensive process for the lender and the homeowner.

See also pre-foreclosure.

Leave a Reply

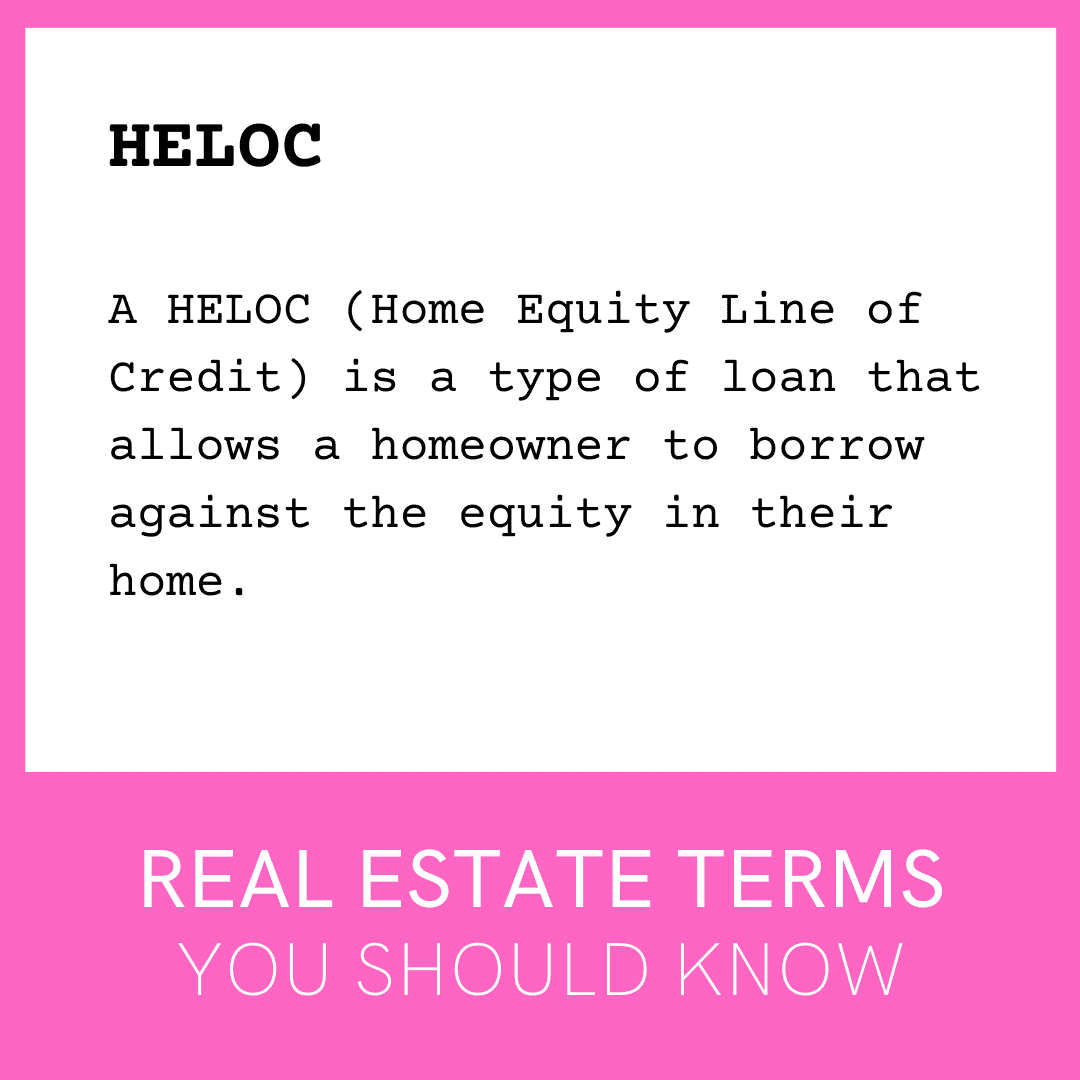

What is a HELOC?

A HELOC (Home Equity Line of Credit) is a type of loan that allows a homeowner to borrow against the equity in their home.

The borrower can use the money for whatever they choose and the interest rate is usually lower than other types of loans.

The loan is secured by the home, so if the borrower can’t make payments, the lender can take the house.

Sometimes a Home Equity Loan is a better choice for the borrower. Talk to your lender to find out more.

Leave a Reply

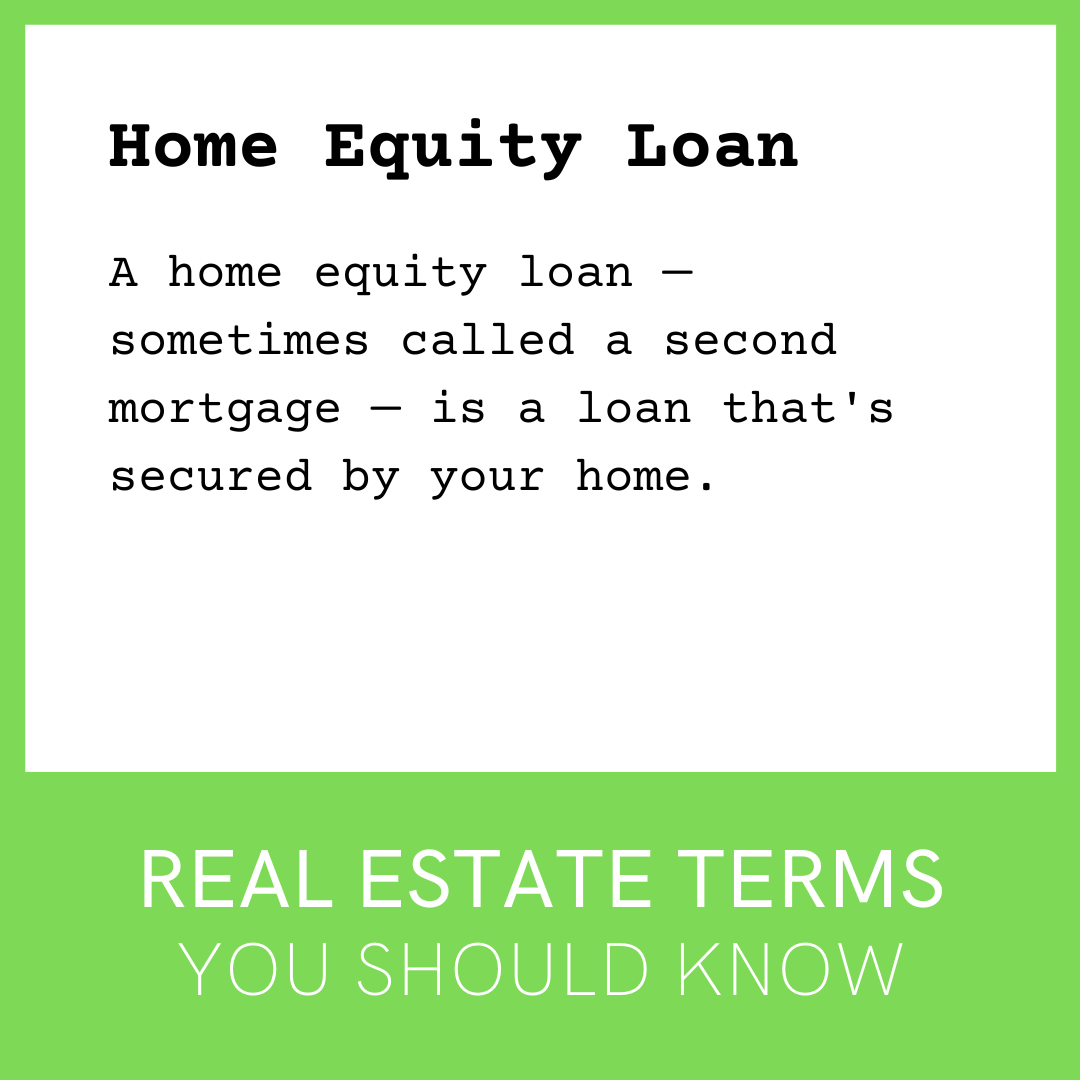

What is a Home Equity Loan?

A home equity loan — sometimes called a second mortgage — is a loan that’s secured by your home.

You get the loan for a specific amount of money and it must be repaid over a set period of time.

You typically repay the loan with equal monthly payments over a fixed term.

If you don’t repay the loan as agreed, your lender can foreclose on your home.

See also HELOC

Leave a Reply

What is a Jumbo Loan?

Conforming loan limits are $647,200 for most of the U.S., so anything above this would be a jumbo loan.

Jumbo loan requirements are stricter and there are more requirements you will need to satisfy.

Find out more about jumbo loans here.

Leave a Reply

What is a lender?

A lender, AKA Mortgage Lender is an entity that issues mortgage loans. Typically, a bank, mortgage broker, credit union, etc.

A mortgage lender is a bank or other financial institution that provides loans to people who want to buy a home.

The lender will look at a person’s credit history, income, and other factors to decide if they are eligible for a loan and how much they can borrow.

The lender will also discuss the different types of mortgages available and the interest rate and terms of the loan.

Leave a Reply

What is a Mortgage?

A mortgage is a loan from a lender or bank that is used to purchase your home. BTW, the “t” is silent, so it’s pronounced “more·guhj”.

A mortgage is a loan that a person takes out to buy a house.

The borrower pays the lender back over time with interest.

The mortgage is secured by the house, which means if the borrower can’t make payments, the lender can take the house.

Mortgages usually have a fixed interest rate and a set term (how long the loan will last).

For instance, a common mortgage is a 30-year fixed loan. That is, the loan lasts for 30 years and the interest rate remains the same over the life of the loan.

Leave a Reply

The interest rate on a mortgage loan you pay to borrow that money when buying a home.

The lower the rate, the better.

Mortgage rates vary daily, so you don’t have any particular rate until the lender “locks in the loan” securing that rate for your home purchase.

The rate you qualify for is based on your personal financial situation and the type of loan you are applying for.

Leave a Reply

What is a Pre-Approval Letter?

It is a letter from a lender indicating you qualify for a mortgage of a specific amount.

Getting Pre-Approved

You’ll fill out a mortgage application, provide documents, and bank statements, get a copy of your credit report, etc.

Getting pre-approved is what you need to do before starting a home search. The person selling your dream home will want to make sure you really are qualified to buy. Most sellers aren’t willing to accept your offer with only a pre-qualification.

Leave a Reply

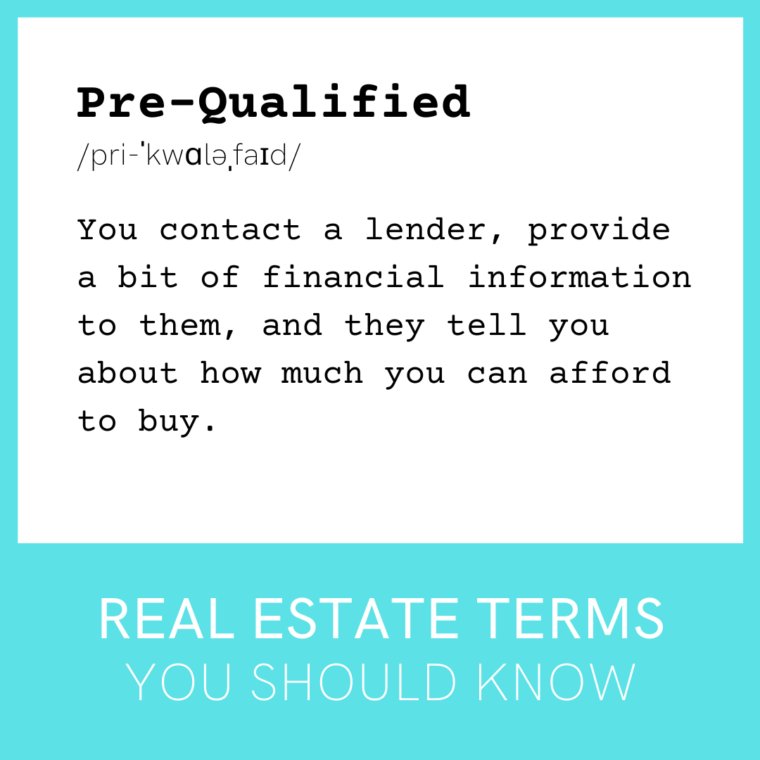

What is getting Pre-Qualified?

You contact a lender, provide a bit of financial information to them, and they tell you about how much you can afford to buy. That’s about it. It’s usually done over the phone, and your credit report is not needed at this point.

WARNING!  It’s NOT a promise of a loan. You are not guaranteed any particular interest rate. And you are not ready to purchase a home. What you have is an idea of what you may be able to buy. It’s a starting point, and a good way to start planning.

It’s NOT a promise of a loan. You are not guaranteed any particular interest rate. And you are not ready to purchase a home. What you have is an idea of what you may be able to buy. It’s a starting point, and a good way to start planning.

You’ll want to get a Pre-Approval Letter from your lender before you start shopping for a home.

Leave a Reply

One of the first steps in purchasing a home is getting either pre-approved or pre-qualified for a mortgage. Unless of course, you’re buying with all cash. 😁

It’s very easy to get confused between the two things. So, should you get Pre-Qualified or Pre-Approved for a mortgage loan?

Without getting into too much detail, we’ll give you just the essentials to understanding the difference, not the complete procedure for each.

Pre-Qualified

This is the simpler of the 2 processes. You contact a lender, provide a bit of financial information to them, and they tell you about how much you can afford to buy. That’s about it. It’s usually done over the phone, and your credit report is not needed at this point.

WARNING! 🔥 It’s NOT a promise of a loan. You are not guaranteed any particular interest rate. And you are not ready to purchase a home. What you have is an idea of what you may be able to buy. It’s a starting point, and a good way to start planning.

Check out Investopedia for a more in-depth explanation if you’re curious. https://www.investopedia.com/articles/basics/07/prequalified-approved.asp

Pre-Approved

This one is where the rubber meets the road. Paperwork, and plenty of it. You’ll fill out a mortgage application, provide documents, bank statements, get a copy of your credit report, etc.

It takes more time and there are more questions. It’s best to start with plenty of time before you plan to start looking for a home. That way you can deal with finding the papers you thought were in that one file cabinet, get your updated investment info, and try to fix any credit issues you may have.

Getting pre-approved is what you need to do before starting a home search. The person selling your dream home will want to make sure you really are qualified to buy. Most sellers aren’t willing to accept your offer with only a pre-qualification.

Again find out more here. https://www.investopedia.com/articles/basics/07/prequalified-approved.asp

Conclusion

Save yourself some heartache, heartbreak, and hair-tearing-out. Get pre-approved before shopping for homes.

Better yet, call me, Libby Guthrie at 925-628-2436 and I’ll answer your questions about getting started, and if you like, I’ll connect you with the right lender for your situation.

Just so you know, before my 25 years as a real estate agent and broker, I spent 15 years in mortgage banking. I know what I’m talking about and I love to share my expertise with you and your family.

Contact me today, share this article with a friend, and please, share it on your favorite social site. Thanks!

Leave a Reply

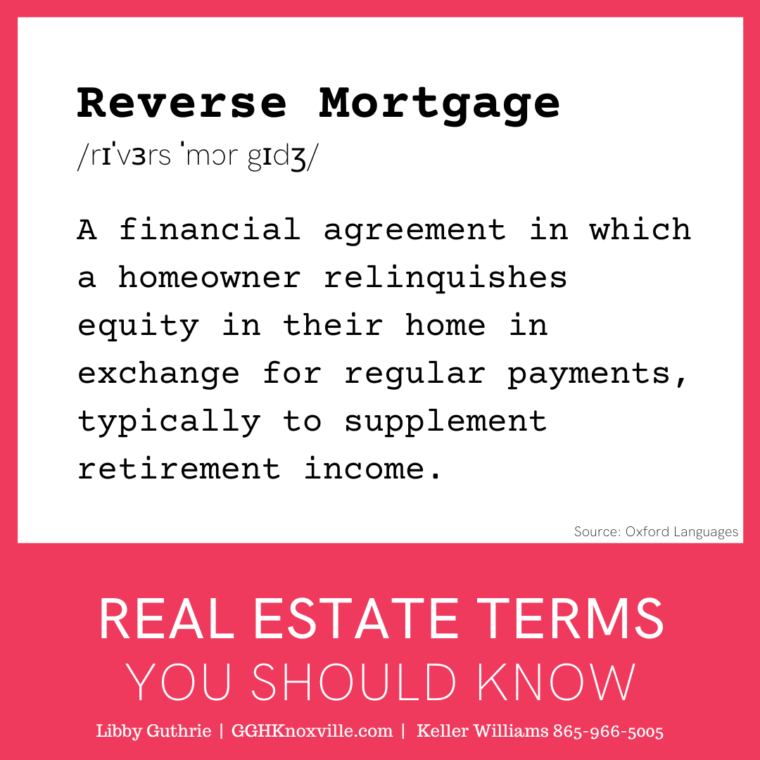

What is a Reverse Mortgage?

A financial agreement in which a homeowner relinquishes equity in their home in exchange for regular payments, typically to supplement retirement income. This type of loan is for seniors ages 62 and older.

Should you get a reverse mortgage?

While it can be a great way to supplement your retirement income, there are some things to watch out for:

⚠️ High fees

To get and finalize your reverse mortgage, you’ll be paying a range of fees that can add up quickly.

⚠️ Variable or high-interest rate

The interest rate is often higher than that of a standard mortgage. It may also be variable, rather than fixed, which means it can increase in the future.

⚠️ Less money for your heirs

The remaining amount of your estate will need to be repaid when you’re no longer here, usually in a specific period of time, which can be costly and stressful for your family.

This is why, in some cases, downsizing can be a better option. If you’re deciding between the two, contact us to discuss your options and make the best choice for your needs.

Leave a Reply

What is a Settlement Statement?

A settlement statement, also known as a HUD-1, is a document that lists all the costs associated with buying or selling a home.

It includes the purchase price, loan fees, taxes, insurance, and any other costs that need to be paid at closing.

This document will be given to the buyer and seller at the closing of the real estate transaction.

Really good agents will also send you a copy of your HUD-1 right before tax time to make sure you take advantage of any tax-deductible expenses from the purchase or sale of your home.

Leave a Reply

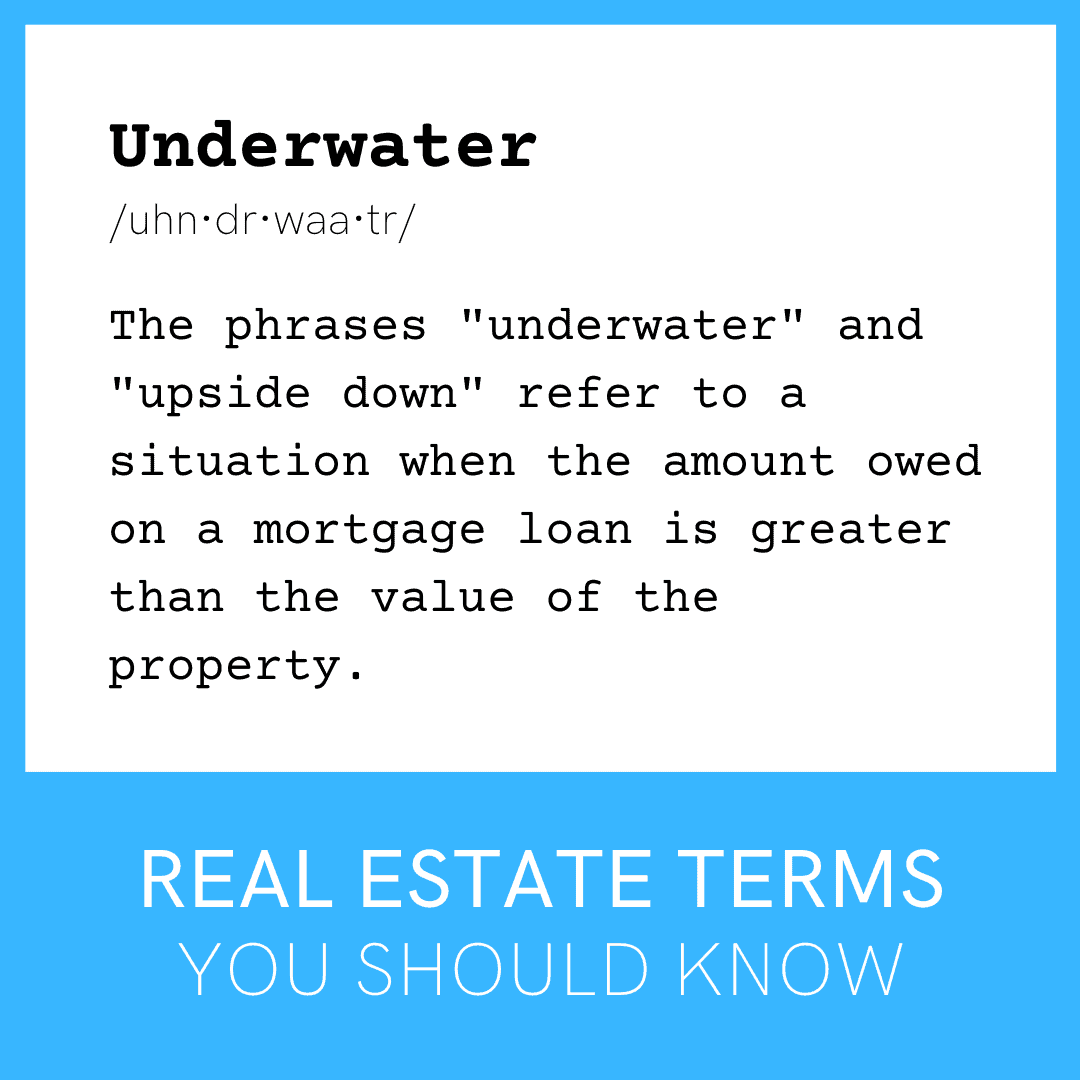

What does it mean when you are Underwater?

The phrases “underwater” and “upside down” refer to a situation when the amount owed on a mortgage loan is greater than the value of the property.

In simpler terms, a house is underwater when the owner owes more on the mortgage than the house is worth.

You have various options on what to do if you are in this situation.

Leave a Reply

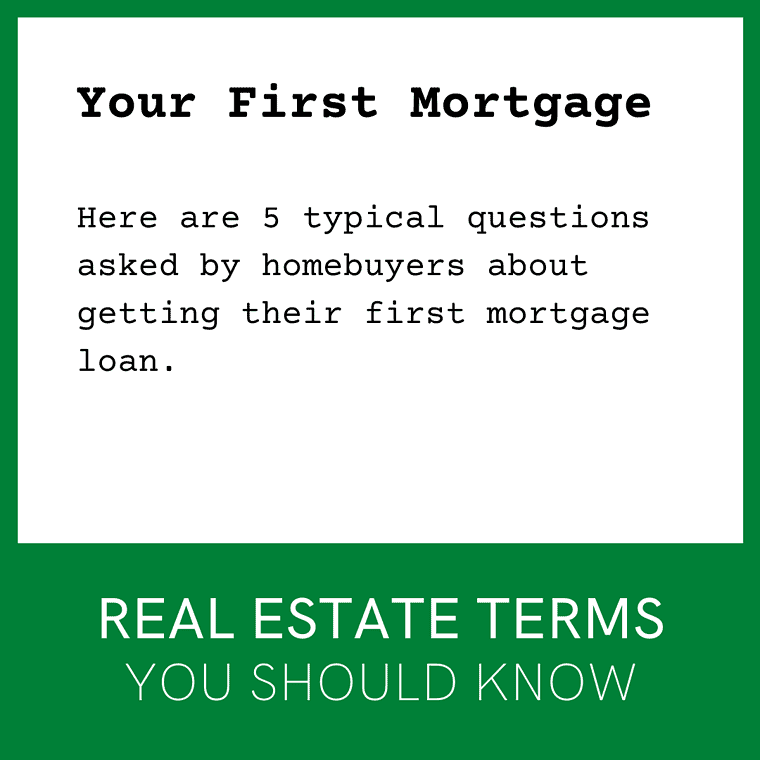

Here are 5 typical questions asked by homebuyers about getting their first mortgage loan.

How much do I need to save up for a down payment?

A conventional loan down payment is usually 20% of the sales price, but other types of financing require as little as 3.5% to 15%. A mortgage lender can tell you what types of loans you qualify for.

How do I know if I qualify for a loan and how much I can afford?

Contact a mortgage lender to get pre-approval for a loan. The lender will ask you some basic questions about your income and debts and can tell you what amount you can be approved for, and how much your mortgage payments will be. Ask me for my lender recommendations!

What does the lender need from me to give me a loan?

Usually, you are asked to provide your last two tax returns to show proof of income. You should also provide recent bank and credit card statements and proof of your current pay rate. You will also be asked for your social security number so they can run a credit check.

The lender may want to meet with you before asking for this documentation, or they may provide you with a list of which documents you need on your first appointment.

What’s the difference between pre-approved and pre-qualified?

While often used interchangeably, these terms don’t mean the same thing. Pre-qualification is an estimate of what you may be approved for based only on the verbal information you provide. Pre-approval means the lender has verified your income and debt information and run a credit check.

Also, read “Pre-Qualified vs Pre-Approved” for more details about the difference between pre-approved and pre-qualified.

How do I know which mortgage option is right for me?

Your mortgage lender is the best person to advise you on this question. Their products and qualifications change from time to time, so they would know best what products are available to meet your needs.

That said, you can always ask me, if you want a second opinion. I began my career in real estate as a mortgage lender.

Leave a Reply

Home Buyers

What is a conforming loan?

A conforming loan is one that is limited to $647,200 for most of the U.S., which means you may be able to avoid the stricter requirements of a jumbo loan.

Loan limits vary over time and by location so you should check with your lender or Realtor for the latest information.

Other loan types include jumbo loans, FHA, and VA.

Leave a Reply

What is a credit score?

A number ranging from 300-850 that’s based on an analysis of your credit history.

Your credit score helps lenders determine the likelihood you’ll repay future debts.

You’ll need a score of 620 or better, but you’ll get better financing rates with a score of 720 or higher.

There is much more to know about credit and credit scores, so feel free to ask if you have specific questions.

To learn more about credit scores and credit reports, click here.

Leave a Reply

What is a Deed of Trust?

A Deed of Trust is like a mortgage. It is an agreement between a borrower (you) and a lender (a bank or other financial institution).

The lender gives you money to buy a house or other property, and you agree to repay the loan with interest, in regular payments.

The Deed of Trust also includes a clause that says if you don’t make the payments, the lender can take the property back.

Leave a Reply

What is a down payment?

The sum in cash that you can afford to pay at the time of purchase of a home or property.

A conventional loan down payment is usually 20% of the sales price, but other types of financing require as little as 3.5% to 15%. Some 0% down programs are also available.

A mortgage lender can tell you what types of loans you qualify for.

Leave a Reply

What is a Jumbo Loan?

Conforming loan limits are $647,200 for most of the U.S., so anything above this would be a jumbo loan.

Jumbo loan requirements are stricter and there are more requirements you will need to satisfy.

Find out more about jumbo loans here.

Leave a Reply

The interest rate on a mortgage loan you pay to borrow that money when buying a home.

The lower the rate, the better.

Mortgage rates vary daily, so you don’t have any particular rate until the lender “locks in the loan” securing that rate for your home purchase.

The rate you qualify for is based on your personal financial situation and the type of loan you are applying for.

Leave a Reply

What is a Pre-Approval Letter?

It is a letter from a lender indicating you qualify for a mortgage of a specific amount.

Getting Pre-Approved

You’ll fill out a mortgage application, provide documents, and bank statements, get a copy of your credit report, etc.

Getting pre-approved is what you need to do before starting a home search. The person selling your dream home will want to make sure you really are qualified to buy. Most sellers aren’t willing to accept your offer with only a pre-qualification.

Leave a Reply

What is getting Pre-Qualified?

You contact a lender, provide a bit of financial information to them, and they tell you about how much you can afford to buy. That’s about it. It’s usually done over the phone, and your credit report is not needed at this point.

WARNING! It’s NOT a promise of a loan. You are not guaranteed any particular interest rate. And you are not ready to purchase a home. What you have is an idea of what you may be able to buy. It’s a starting point, and a good way to start planning.

You’ll want to get a Pre-Approval Letter from your lender before you start shopping for a home.

Leave a Reply

One of the first steps in purchasing a home is getting either pre-approved or pre-qualified for a mortgage. Unless of course, you’re buying with all cash. 😁

It’s very easy to get confused between the two things. So, should you get Pre-Qualified or Pre-Approved for a mortgage loan?

Without getting into too much detail, we’ll give you just the essentials to understanding the difference, not the complete procedure for each.

Pre-Qualified

This is the simpler of the 2 processes. You contact a lender, provide a bit of financial information to them, and they tell you about how much you can afford to buy. That’s about it. It’s usually done over the phone, and your credit report is not needed at this point.

WARNING! 🔥 It’s NOT a promise of a loan. You are not guaranteed any particular interest rate. And you are not ready to purchase a home. What you have is an idea of what you may be able to buy. It’s a starting point, and a good way to start planning.

Check out Investopedia for a more in-depth explanation if you’re curious. https://www.investopedia.com/articles/basics/07/prequalified-approved.asp

Pre-Approved

This one is where the rubber meets the road. Paperwork, and plenty of it. You’ll fill out a mortgage application, provide documents, bank statements, get a copy of your credit report, etc.

It takes more time and there are more questions. It’s best to start with plenty of time before you plan to start looking for a home. That way you can deal with finding the papers you thought were in that one file cabinet, get your updated investment info, and try to fix any credit issues you may have.

Getting pre-approved is what you need to do before starting a home search. The person selling your dream home will want to make sure you really are qualified to buy. Most sellers aren’t willing to accept your offer with only a pre-qualification.

Again find out more here. https://www.investopedia.com/articles/basics/07/prequalified-approved.asp

Conclusion

Save yourself some heartache, heartbreak, and hair-tearing-out. Get pre-approved before shopping for homes.

Better yet, call me, Libby Guthrie at 925-628-2436 and I’ll answer your questions about getting started, and if you like, I’ll connect you with the right lender for your situation.

Just so you know, before my 25 years as a real estate agent and broker, I spent 15 years in mortgage banking. I know what I’m talking about and I love to share my expertise with you and your family.

Contact me today, share this article with a friend, and please, share it on your favorite social site. Thanks!

Leave a Reply

What is a Settlement Statement?

A settlement statement, also known as a HUD-1, is a document that lists all the costs associated with buying or selling a home.

It includes the purchase price, loan fees, taxes, insurance, and any other costs that need to be paid at closing.

This document will be given to the buyer and seller at the closing of the real estate transaction.

Really good agents will also send you a copy of your HUD-1 right before tax time to make sure you take advantage of any tax-deductible expenses from the purchase or sale of your home.

Leave a Reply

Home Sellers

Conventional sale: When the property is owned outright and has no mortgage.

Conventional sales are often smoother transactions than those that require financing as there is no dependence on the buyer receiving a loan to purchase the property.

A conventional sale is not to be confused with a conventional loan. In this instance:

“Conventional” just means that the loan is not part of a specific government program. Conventional loans typically cost less than FHA loans but can be more difficult to get.

This may sound confusing, so just ask your Realtor to explain it to you if you’re not clear. ☺️

Leave a Reply

What is a Settlement Statement?

A settlement statement, also known as a HUD-1, is a document that lists all the costs associated with buying or selling a home.

It includes the purchase price, loan fees, taxes, insurance, and any other costs that need to be paid at closing.

This document will be given to the buyer and seller at the closing of the real estate transaction.

Really good agents will also send you a copy of your HUD-1 right before tax time to make sure you take advantage of any tax-deductible expenses from the purchase or sale of your home.

Leave a Reply

What does it mean when you are Underwater?

The phrases “underwater” and “upside down” refer to a situation when the amount owed on a mortgage loan is greater than the value of the property.

In simpler terms, a house is underwater when the owner owes more on the mortgage than the house is worth.

You have various options on what to do if you are in this situation.

Leave a Reply